Can You Cover the Unexpected Bad Day?

Budgeting doesn’t sound like fun? It really isn’t. But what a difference budgets can make in financial security, especially when you meet the inevitable rainy day or unexpected need.

I don’t really know anyone who loves to budget – it’s like being on a diet. But unlike a diet, your budget isn’t about denying yourself. It’s more about taking control and choosing how you want to spend your money. So, it’s a “spending plan”…and evidently more of us should be using one. Consider this: 6 in 10 Americans say they don’t have enough savings to cover an unexpected expense of $500 to $1,000, according to a February, 2017 survey at Bankrate.com.

A spending plan affords several benefits:

- See where your money goes (are these your priorities?)

- See where you can cut (too much going out?)

- Have some to save and invest (for things you really want)

- Build a “rainy day” stash (for that unexpected emergency)

- Get out of debt faster (and save on financial fees)

It doesn’t need to be complicated or take a lot of time to make a good spending plan. Use a pencil and paper, or if you like spreadsheets, start there.

If money is tight (you’re a student, have erratic income, live paycheck to paycheck, lost your job), do a monthly or weekly budget. If you have a good handle on your finances and things don’t change much, an annual (12 months) plan might work well for you.

Where does a plan start?

A budget is a plan where every dollar is earmarked, or put in a category, so your spending plan needs these two basic columns:

- Cash coming in = your income from paychecks, bonuses, dividends, tips, alimony received, etc.

- Cash going out = your expenses to pay, plus debt repayment and something for savings

Budgeting forms often follow a spreadsheet format. They can look very serious, with detailed expense categories and sub-categories and dollar amounts for each. If this works for you, by all means, use it. But you can also opt to use percentages rather than fixed amounts for each expense item.

This doesn’t mean you cut out some smaller expenses or don’t account for every dollar. But rather than agonize over adjusting dollars and cents, percentage budgeting focuses on the big picture – how much of the pie each expense category eats up.

For example, here are expenses categories you might include:

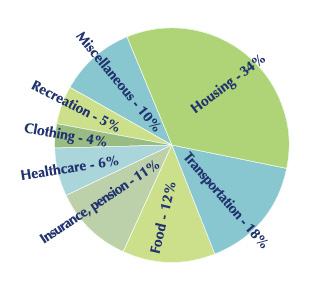

- Housing (rent, mortgage, utilities)

- Transportation (including car loan)

- Food (groceries and restaurants)

- Insurance, pension, 401k (portions you pay)

- Medical/Health care

- Clothing

- Entertainment/Recreation

- Miscellaneous (personal items, cell phone)

- Debt repayment (student loan)

This pie chart shows the average percentages for common expenses annually, based on statistics from the Bureau of Labor:

If you are adding in loan repayment, adjust your percentages to allow for 7-10% for a new category. But for payments on a credit card, only the interest and fees would go in this repayment category (you would include each credit card purchase in the appropriate expense category).

If you want to use an app rather than pencil and paper, you could check out Mint, GoodBudget, LearnVest, or Personal Capital.

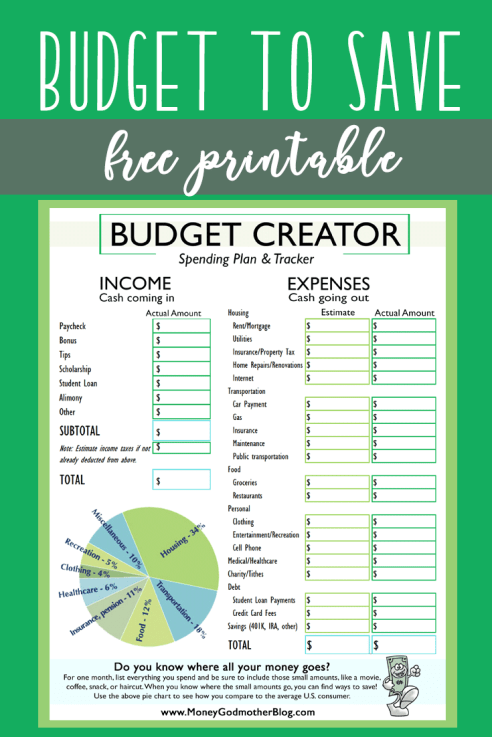

To easily create your own spending plan, get the Money Godmother’s free printable, Budget to Save. Click this free budget printable link to print!

Leave a comment