How to Be Credit Smart for a Lifetime

So you’ve checked your credit score lately? It’s trendy these days, and more consumers obsess over tracking it. But do you know how to apply what a score reveals?

There’s more to being smart about credit than a single score. Yet more Americans than ever check for that score. And while those scores have gone up slightly, our credit knowledge has been eroding – at its lowest point in the last 8 years, says an industry survey. At the same time, the debt load that consumers carry has steadily risen, to a record $4.09 trillion in May, according to Federal Reserve data.

This sounds like a recipe for impending disaster.

As the 9th annual Credit Score Knowledge Survey indicates, “consumers know less about credit scores but think they know more,” said Stephen Brobeck, Consumer Federation of America (CFA) senior fellow. The 2019 survey was released in June by CFA and VantageScore Solutions LLC, the independent credit scoring company started by the Equifax, Experian, TransUnion credit reporting agencies.

Why Covet a High Credit Score?

It’s no secret how much lower credit scores do cost you – impacting everything from your loan terms, credit card limits, insurance rates and deposit amounts, and resulting in hundreds, or even thousands more in higher loan and service fees. But must you have a perfect credit score or be in constant pursuit? If you need to borrow money, a higher score is advantageous.

But remember that score is a fleeting snapshot in time – it changes frequently, based on your transactions. Each time you swipe your credit card to pay for a purchase, the amount extended to you is considered a loan until it’s paid off (hopefully the due date of the credit card bill). So using those cards responsibly is crucial.

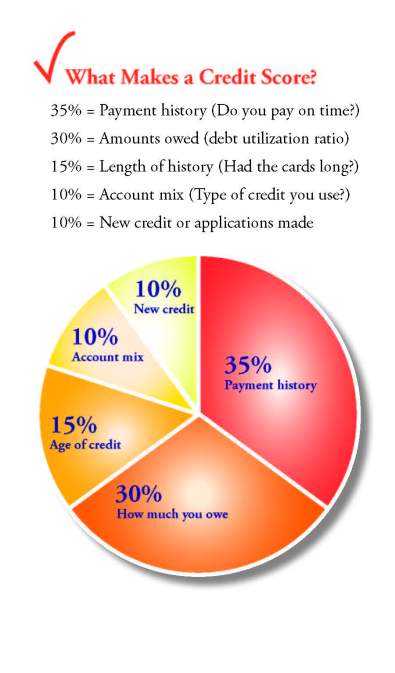

Plus you should know that, in addition to bankers and credit card issuers, others check your credit history – employers, landlords, insurers, and phone companies, to name some common inquirers. They’re looking for key data that indicates how reliable you are and assessing you as a financial risk to them. This info includes the basics of a credit score:

Credit is a Tool, Not a Cash-Flow Strategy

An Experian survey using data from Q1 2019 shows average consumer debt balances peak at age 45 and begin to decline as people grow older. But the average balance is inching up. Increases in the credit card balances for U.S. consumers, by age range are:

- Gen Z (ages 18-22) = $2,057, up 11%

- Millennials (23-38) = $4,712, up 7%

- Gen X (39-54) = $8,023, up 3%

- Boomers (55-73) = $6,788, down 1%

If you need to raise your score, here’s a guide to do just that. Maybe you feel you’ve already mastered your cards? Check your credit smarts with these three steps:

- To see how much you know, take this simple quiz.

- Check your credit history (free annually) at the official government site or call 800-322-8228.

- Manage each life stage of credit challenges – check your to-do list below:

If you’re younger than 30…Start building a good credit history:

- Note why you’re applying for a credit card and how to use one responsibly

- Understand credit card terminology, especially the cash advance feature

- Research card options and terms before applying

- Choose a card you want to keep a couple of decades or more

- Opt for a card with no annual fee

- Understand and read each credit card bill you receive

- Pay your bill in full – and on time – every cycle

- Keep tabs on your financial life (there are plenty of tech tools to do this!)

- Check your credit transactions – as often as you check Facebook or Instagram – to avoid fraud and identity theft

In your 30s, 40s and 50s…Maintain a great score, reduce debt:

- Keep utilization ratios low as your credit limit grows

- Keep managing credit responsibly to get better rates when borrowing for a house, car, vacation home or other major purchase

- Make it a goal to build wealth not debt

- Pay off debt rather than transfer a balance to a new card

- If you add new credit cards, keep spending in check and don’t use more credit than you can afford

- Strive to pay your credit card bill in full and on time every cycle

- Monitor your financial accounts, especially watching for fraud and identity theft

When you’re over 60…Time to wean yourself from credit:

- Reduce your reliance on borrowing, aim for financial independence

- Pay credit card bills in full and on time, every cycle

- Opt to use fewer cards

- Remain diligent about checking your accounts and credit history

- Be aware that scam artists particularly target older adults

- Pay off mortgages or other loan balances as soon as possible

- Strategize to plan a retirement lifestyle that does not rely on credit

While using credit responsibly is a life skill that can help you acquire assets, remember the bottom line is about making wise financial choices to build wealth. Credit is only a tool, not a cash-flow strategy.

Leave a comment