Credit: The More You Use, the More You Know?

More Americans than ever are using credit…AND checking their credit scores. Is it really a big deal to always know your credit score? Does what’s in your wallet matter?

What a difference a score makes, especially when you want to borrow money.

A lower credit score typically means less attractive loan terms and paying hundreds – or thousands – more in loan interest and fees. Your score also affects your credit card interest rates, insurance rates and deposit amounts for mobile phones and utilities. It might even cost you a job.

Yes, credit scores have become a big deal. While they began as a lender’s measure of how risky it was to loan money to a particular borrower, credit scores have since become a yardstick for determining so much more. For example, employers and landlords often count on credit scores to judge character and reliability.

Do You Have Good Credit?

According to the common scoring yardstick…

- A = 750 +

- A- = 725-749

- B = 700-724

- C = 650-699

- D = 600-649

- F = Below 600

So naturally, you want to know if you have an A, right?

Inquiring Minds Want to Know

Not surprisingly, the number of Americans who obtained credit scores jumped to 57% this year. This compares to just 49% in 2014, according to the 2018 Credit Score Knowledge Survey by the Consumer Federation of America (CFA) and VantageScore Solutions (the independent credit scoring company founded by U.S. credit reporting bureaus Equifax, Experian, TransUnion).

You’ve probably seen plenty of websites advertising access to your credit score. Before you click to get a score, realize that many websites also want to sell you something and that your score changes constantly, as you use your credit. Your score today will not be the same a month from now.

What you really might want to see is your credit report, a history of your credit actions. You can get this credit history free from TransUnion, Equifax and Experian every year at the government site, www.annualcreditreport.com or call 800-322-8228. (Report is free, you pay to get a score.)

And…you might be curious how you compare.

Are You a Typical Credit User?

Check this credit snapshot from Experian data (2017):

- 675 = Average VantageScore (highest since 2012)

- 22.3% = Americans with scores of 781-850 (great!)

- 21.2% = Americans with scores below 600

- $201,811 = Average mortgage debt

- $ 24,706 = Average non-mortgage debt

- 5.6 = Average number of credit cards

- 3.1 bank cards, with average balance of $6,354

- 2.5 retail cards, with average balance of $1,841

Remember this snapshot averages “typical” across the U.S., lumping together various geographic, housing, and cost-of-living differences. (For a state-by-state look, check this infographic.)

We’re Using More Credit

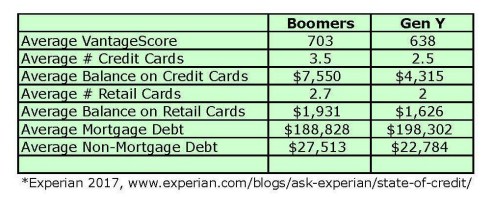

On average, data indicates Americans’ credit card debt jumped almost 3% from last year — to $6,354, up from $6,188. Younger demographics saw sharper rises: Millennials’ credit card debt climbed 10.8%, to $4,315, while plastic debt among the Boomers stayed almost flat.

You might be curious how “typical Boomers” compare to “typical Millennials” overall…

A Generational Look at Credit Use

What Comprises Your Score?

Your credit history is used to generate a score when a lender requests one. These factors determine a score:

- 35% = Payment history. So, PAY BILLS ON TIME.

- 30% = How much you owe, amount of credit limits vs. amount you use. The lower your debt usage, the higher your score.

- 15% = Age of credit, longer is better. Do you know when you opened your oldest credit card?

- 10% = The more new credit you apply for, the lower your score.

- 10% = Account mix, or what type of credit are you already using? This includes revolving credit (cards) and installment credit (a car loan, mortgage).

Here’s the weight given to each factor:

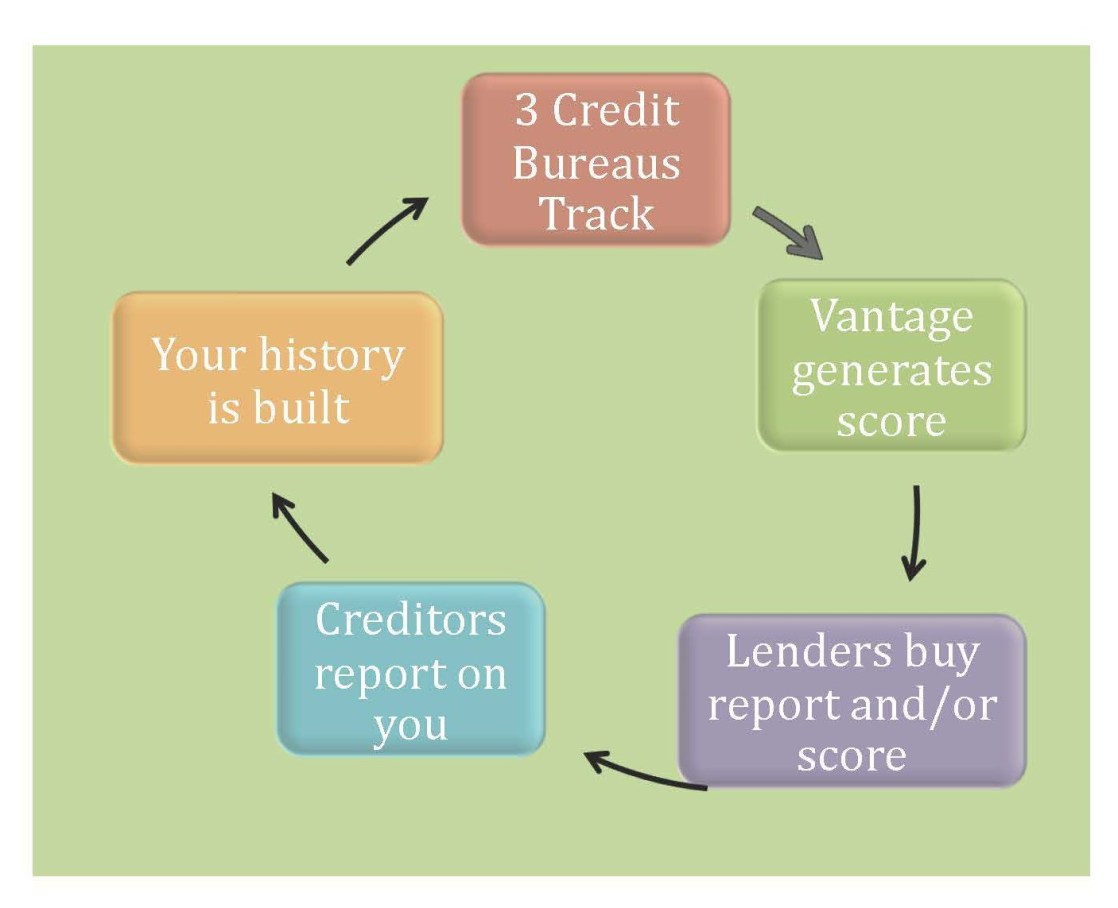

Watch Your Credit Journey Unfold

Here’s how your credit transactions follow you…the rest of your life:

Find more MoneyGodmotherBlog.com articles about credit here and here.

Leave a comment