Why Having a Savings Account Matters

Do you have at least one savings account? Okay, interest rates are paltry. So why bother with regular savings accounts? Why not just let that idle cash set in your checking account? You’re missing out on building a key habit.

Using savings accounts and developing the skill to regularly set aside money are learned habits.

Do you have just one savings account or one for each goal (vacation, college, wedding, new car, etc.)? Do you have a savings account for yourself, your children, your grandchildren? It’s never too early!

Unfortunately, many don’t.

In fact, 24.5 million households do not have any account at an insured institution (like a bank), according to a survey by the FDIC, Federal Deposit Insurance Corp. As in previous surveys, the most common reason respondents did not use a bank (more than half) was they believed they didn’t have enough money to bother having an account. Really?

Folks, you can’t win when you don’t play!

Why It’s Important to Have a Savings Account

Not having that pipeline to save regularly – a savings account – makes it hard to do the transactions to save and build wealth (or even get attractive credit terms for some). Though many have the ability to save, they have no way to execute. Therefore, they don’t.

You’ve probably seen those stats showing that so many consumers don’t have enough money to cover an emergency, haven’t saved an adequate nest egg or don’t bother to fund their 401k at work?

- About 6 in 10 say they could not cover a $400 emergency expense (Federal Reserve 2016 Report on Economic Well-Being)

- Only about 47% of adults said they are able to save part of their annual income (Federal Reserve)

- In 2016, only 44% workers participated in a company-sponsored retirement plan (U.S. Bureau of Labor Statistics)

Notice these all relate to developing that basic savings habit – regularly setting aside a bit of money. In each case, starting early with a savings account can help you smooth out some of life’s unexpected bumps.

So, open a savings account, no matter how small.

Saving Money Saves You Money

By having a cushion of savings, you can also avoid the costs of borrowing money, paying to cash a check, paying interest on credit card balances and/or using payday lenders.

Not having money saved costs you at every turn.

The FDIC survey indicates about one of every four households used alternative financial services in 2015—a payday loan or non-bank, check-cashing service.* Households with more volatile incomes were more likely to use these services, even households with higher levels of income. Why? They had no savings banked for an emergency – no cushion!

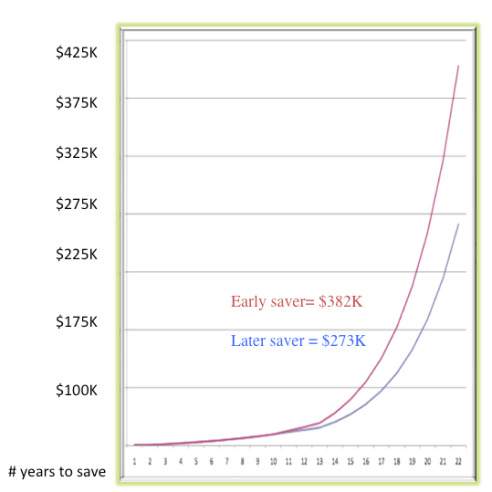

Small Amounts Add Up – that’s the magic of compounding

Just like many habits, learning to save is often easier when you start sooner. While your savings might be slow to grow when you’re really young and don’t have a steady paycheck, even small amounts can snowball and become a sizable nest egg.

Here’s my tale of two savers (all things equal, including identical paychecks and interest rates on savings) who made just slightly different decisions about when to save:

• The early saver puts in $20 per week for 10 years and then stops = about $10,000 total

•The later saver waits (starts saving when the other saver stops), but puts in $60/week for 20 years (twice as long) = about $62,000 total

• Yet, the power of compounding gives the early saver an enormous advantage

In this case, the late saver saved much more and for more years, but couldn’t catch up.

Which saver do you wish to be? Wouldn’t it more fun to have your money do the work for you, rather than you working for every dollar you put in? Starting your savings early gives the power of compound interest time to work.

Just get started….today!

So Pay Yourself First – that means stash away savings before you pay bills

One of the best ways to build your savings nest egg is putting it on auto-pilot – sock away something by automating that transaction to happen with each paycheck.

Using a savings account is:

- Economical – you can usually find a “no-fee” account

- Safe – protected from loss or theft by FDIC insurance (or NCUA for credit unions)

- Efficient – by automating deposits from your paycheck direct to savings account

- Leverage-able – can be collateral for loan, shows your capacity, reliability

- Less hassle – connect your online accounts, use your bank’s mobile app

- Accessible – you can withdraw money if you need it, immediate liquidity

- Passive income – you get paid interest on your savings

- Credit reduction – you may be able to pay cash instead of borrowing for a major purchase (save on interest, loan costs)

Savers Become Investors – the path to building wealth

Those who become adept at saving often seek better rates of return, so they want to invest rather than just use a savings account. Just remember this greater reward comes with greater risk…you can lose money you invest but savings in a bank account is protected by the FDIC. More on investing accounts later!

*When FDIC did the first survey in 2009, it was the most comprehensive look at the unbanked and under-banked households ever undertaken. The survey is based on responses from roughly 36,000 households.

Leave a comment